(Stata13): VAR Estimation and Discussions #var #Johansen #lags #serialcorrelation #normality CrunchEconometrix 13:36 6 years ago 52 392 Скачать Далее

(Stata13): VAR and Impulse Response Functions (2) #var #irf #impulseresponse #innovations #shocks CrunchEconometrix 9:12 6 years ago 41 621 Скачать Далее

(Stata13): VAR Estimation and Diagnostics #var #Johansen #lags #serialcorrelation #normality CrunchEconometrix 5:21 6 years ago 16 567 Скачать Далее

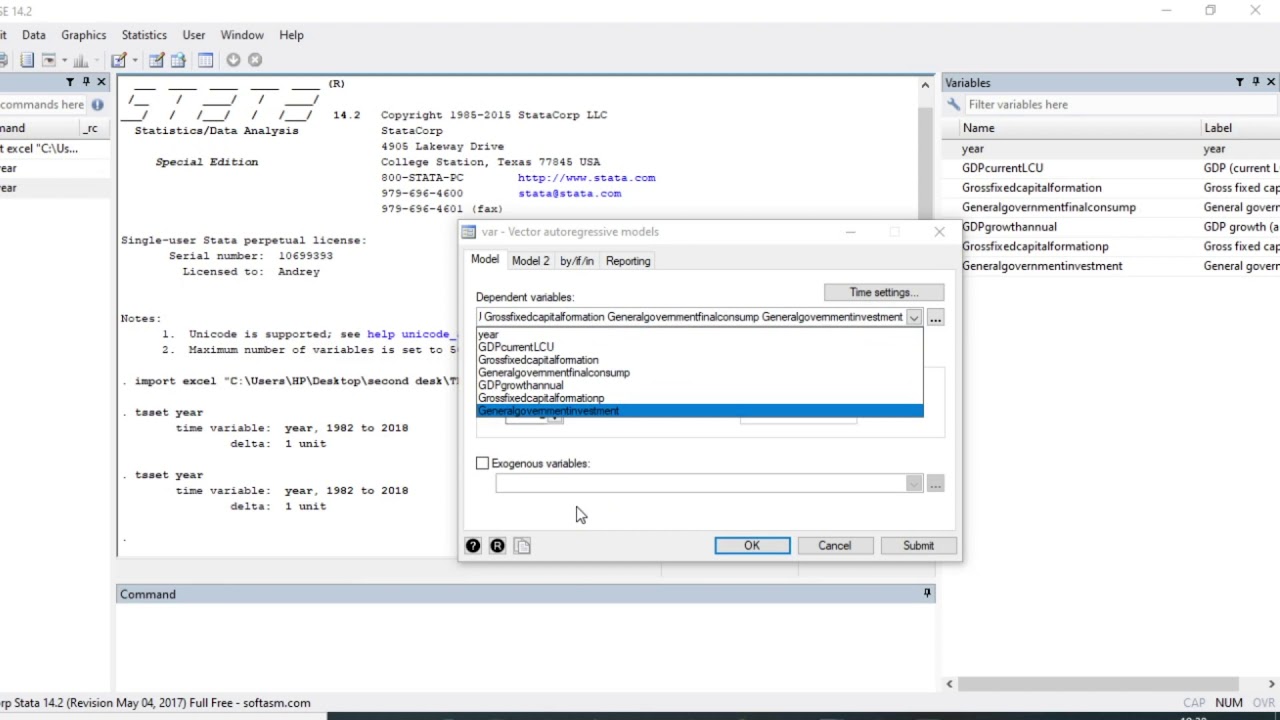

How to run and interpret Var model in STATA Statistical Models for Social Sciences 7:46 3 years ago 13 511 Скачать Далее

(Stata13): VAR and Impulse Response Functions (1) #var #irf #impulseresponse #innovations #shocks CrunchEconometrix 5:18 6 years ago 10 895 Скачать Далее

(EViews10):Estimate VAR Models(1) #var #vecm #Johansen #normality #serialcorrelation CrunchEconometrix 5:27 6 years ago 29 671 Скачать Далее

(Stata13): VECM Estimation, Discussion and Diagnostics #var #vecm #causality #granger #wald CrunchEconometrix 19:05 6 years ago 71 507 Скачать Далее

How to estimate and interpret VAR models in Eviews - Vector Autoregression model JDEConomics 14:57 3 years ago 71 911 Скачать Далее

Running Panel Var models in Stata- Panel Vector Autocorrection (PVAR) Model full Tutorial Noman Arshed 8:54 10 months ago 4 905 Скачать Далее

(Stata13): How to Perform Johansen Cointegration Test #var #vecm #Johansen #cointegration CrunchEconometrix 9:12 6 years ago 43 558 Скачать Далее